Each year as the calendar changes and high school students begin thinking about their next steps, many considering college find themselves at a loss for how to pay for all of the tuition, fees, room and board, books, and more that come with stepping out and into the “real world.”

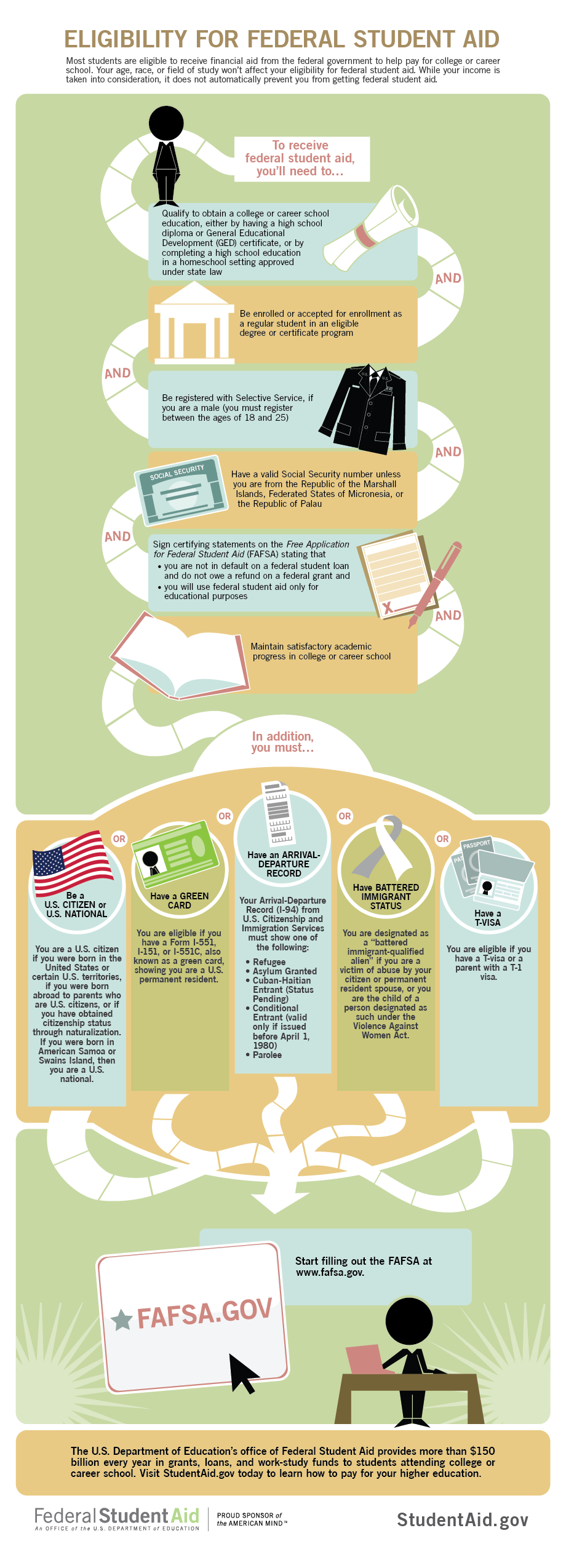

Most students look first at the Free Application for Financial Student Aid, or FAFSA, which is a great place to start. However, FAFSA money can dry up very quickly, and is generally provided to students on a first-come, first-serve basis. In short, this means that if you wait to apply in the spring or summer, you likely won’t get as much FAFSA money as you would by applying early on.

Whether you applied too late or simply weren’t eligible for enough financial aid to cover the cost of college, it’s important to understand what the best FAFSA alternatives are. The truth is, there is a lot of financial aid available, especially to high-achieving and minority students, so it’s good to know where to look when the time comes.

FAFSA First, Other Sources Second

There is no way around the fact that, for most college students, submitting a FAFSA application in the beginning of January is a good strategy. In fact, some states have early deadlines meaning those who apply before March 30th may receive double the grant money that late filers get.

There is no way around the fact that, for most college students, submitting a FAFSA application in the beginning of January is a good strategy. In fact, some states have early deadlines meaning those who apply before March 30th may receive double the grant money that late filers get.

We’ve discussed how and why college-bound students should apply for FAFSA before, and Time Inc. has some great suggestions for how to get the most FAFSA money, including paying down bills before applying, shielding investments that you don’t need to list, or being strategic in how you order your colleges of choice. Using a few of these tactics may increase your award amount.

Get Free Help With FAFSA

Experts say the FAFSA process is much simpler today than it was when I was in college, but it’s still a process that requires a lot of documentation and attention to detail.

Experts say the FAFSA process is much simpler today than it was when I was in college, but it’s still a process that requires a lot of documentation and attention to detail.

Fortunately, there are a few organizations that can help you through the process. Two such organizations, College Goal Sunday and College Week Live host live or online events where they offer free professional assistance and advice for those filing FAFSA applications.

Don’t go it alone and risk making mistakes that reduce your eligibility, use the available resources to your advantage.

Ask Your High School Counselor

Most high school programs offer some level of guidance services for students, especially those nearing graduation. Because these services are provided to all students at a school (where offered), this is one of the first places you should look.

Your guidance counselor, if available, should be able to point you to a number of resources and provide advice based on past experience with other graduating students.

Check With Your College/University’s Financial Aid Office

When your FAFSA application has been submitted, it’s time to start looking for other sources of aid.

According to Cristena Jenner, guidance counselor at The Keystone School, the college or university you choose may have funds available, but you might have to seek them out.

“Students can contact each college’s financial aid office to see if they have college-specific scholarships the students may be able to apply for. Some colleges use the CSS/Financial Aid PROFILE to help to award non-federal financial aid.”

Laurel Barrette, director of guidance counseling services at K12 recommends scheduling an appointment with an advisor rather than speaking with the person at the front desk.

There are a few reasons why speaking to an advisor is a good idea.

First, an advisor often has a little more wiggle room than someone in reception that handles common questions all day. An advisor, for example, can sometimes make exceptions for students who have an ill parent, a difficult or changing tax situation, or other extenuating circumstances that result in financial need.

Explore your options, but understand that the school doesn’t “owe” its students anything. Being polite and respectful towards the people who can help you can make all the difference when it comes time to decide who gets what aid from the school.

Use Third-Party Scholarship Sites

If you’ve already completed your FAFSA application and reached out directly to the college or university that you’ll be attending, fastweb.com, scholarships.com are other similar scholarship sites that offer large databases of scholarships from a variety of sources.

The sources are diverse and include some oddly-specific scholarship foundations, including the Asparagus Club Scholarship for students majoring in business, food management, or the grocery industry. There may be a scholarship out there for any student, you just might have to do some digging .

Earn a Paycheck

In addition to aid from other sources, many students should consider finding work and paying out of pocket for some costs, particularly when faced with a financial aid gap that could result in borrowing money to pay for school.

Even a part time job over a summer can earn a couple thousand dollars, helping to offset the cost of tuition, fees, and books, but working full-time when not in school is even better.

While it’s possible to work part or full time when not attending classes, many students should also try to find part-time work (10-20 hours/week) during the school year. Even if it means taking a lighter course load and tacking on year or two, paying for school as you go can save you a lot of money and trouble down the road. College programs don’t need to be completed in the four years generally allotted, especially if it means that you can avoid student loans.

One of the best places for students to find employment is through the Federal Work Study program according to Laurel Barrette. Another is Americorps, an often-overlooked resource for student employment.

If working part time during school isn’t an option for you, consider a gap year between high school and college, or if you can, between college years. Taking a break from school to focus on padding your bank account can be a great way to keep your plans moving, even if it means taking a little longer.

Working during college isn’t for everyone, but it can save you from debt later in life. Every dollar earned is a dollar not borrowed, which is becoming increasingly important as student loan debt soars. Don’t get caught in the cycle that millions of students have fallen into over the last few decades, I guarantee you will thank yourself later.

Reduce Your Costs

While it’s great to seek out sources of financial aid that can help you get through your college or university program of choice, cost reduction is something that more and more students are looking into as tuition rates continue to increase at record levels.

Before graduating high school, students can earn credit towards a degree by participating in a number of early college programs such as Advanced Placement (AP®) courses or dual-enrollment at a local community college. This route can provide thousands of dollars in benefits down the line, but if you’re already of out of high school or graduating soon, your focus will be on reducing costs while enrolled in a college program.

When asked to describe changes in college attendance patterns related to rising costs, Christena Jenner noted some new trends:

“More students are attending community colleges. I also notice more students seeking a gap year to work or earn money before applying to college. I have also noticed that students who have a higher financial need apply to more schools. Federal Financial Aid is based off of Cost of Attendance (which varies by college) minus Expected Family Contribution. That determines the federal award you may get.

Then, colleges will see what non-federal financial aid they can provide to the student. Students who are seeking the lowest tuition possible seem to apply to multiple schools, then ‘shop’ for the most affordable option once the financial aid reports start arriving.”

Considering an in-state school or community college instead of your dream program can save you tens of thousands of dollars per year. In fact, staying close to home not only means you’re paying in-state tuition, but many students are choosing to live at home with their parents for a few years after graduating high school to save money on room and board.

There are many ways to reduce the overall cost of college, whether it be lower tuition or lower room and board. It’s important to consider your options and choose a path that offers the greatest chance of success later in life, even if that means staying closer to home for the first year or two of college.

Borrowing is Still an Option, But Do It Right

Many students choose to finance their education with loans, but debt really should be looked at as a last resort considering all of the great ways to save and pay for college listed above.

The truth is, however, not all borrowing is bad, and certainly not all loans are created equally.

If attending college costs you an average of $20,000 per year, and you’re able to cover $15,000 each year through working, or earning grants and scholarships, that could get you out of college with a loan payment around $100/month ($20k debt, 5% interest rate, 30 year payment schedule) depending on how long it takes to complete your degree.

Federal Direct Loans

The best loans for students tend to be government subsidized loans like Federal Direct Loans. The U.S. Department of Education pays the interest on Direct Subsidized Loans:

- while you’re in school at least half-time,

- for the first six months after you leave school (referred to as a grace period), and

- during a period of deferment (a postponement of loan payments).

While subsidized loans are typically given to students who need aid the most, nearly all students can get Federal Direct unsubsidized loans (the difference being that the student must pay the loan interest while in school).

You can learn more and find the application for such loans on the Federal Student Aid website.

PLUS Loans

PLUS loans are also provided by the U.S. Department of Education, but the major differences between Federal Direct and PLUS loans are that PLUS loans are funds for parents to borrow to help their children pay for college, and repayment generally begins shortly after the funds are disbursed, rather than post-graduation.

These loans are typically awarded to parents that have good credit. Interest rates for PLUS loans are

Perkins Loans

Another good U.S. Department of Education loan option is the Perkins Loan.

The major difference between Federal Direct and Perkins loans is that the Perkins loan is designed for students with exceptional financial need. Interest rates are capped at 5%, meaning you won’t get a major case of sticker shock when that first loan payment comes due.

Not all schools participate in the Perkins loan program, so check with your financial aid office to find out whether this is a good option for you.

Private Loans: Beware!

The truth of the matter is that when you’ve exhausted all other options, there are plenty of private organizations that are willing to loan you money for school, but typically at a higher interest rate than federal loans, and possibly with more fees as well.

Private loans should be carefully considered. Sure, they can be what a student needs to get through those last few semesters of college, but because private loans are generally more expensive, they should be the last loan option that students look at.

There are a few sites out there that make it easier to find lenders that offer the most favorable terms, one such organization is SimpleTuition. This service offers you the ability to compare private loan options to find which fits your needs the best, and it’s possible to save thousands of dollars over the repayment period by finding the best loan.

I ran a quick search on SimpleTuition and found that the repayment cost for a $10,000 loan at today’s rates would cost somewhere between $11,201 and $30,895 depending on which lender I selected.

If that’s not proof that shopping around can save you money, I don’t know what is!

What Does This All Mean?

Many people these days are questioning whether going to college is worth it anymore. Some people feel that high school graduates are better off going straight to work out of high school and developing skills in their preferred career field, especially when faced with rising tuition costs and ballooning debt.

In fact, the average college graduate now enters the workforce with nearly $30,000 in student loan debt due, in part, to skyrocketing tuition costs and overeager lenders. When you look at all of the college graduates in the U.S. who are currently repaying loans, that adds up to a staggering $1.2 trillion in student loan debt. That. Is. Nuts.

That’s not to say that high school graduates can’t enter a trade school and make a decent, honest living. Plumbers, for example, make an average of $49,000 per year (with potential to make much more) and no lengthy college program is required to enter the field.

But looking at the bigger picture, it is becoming more and more difficult for high school graduates to compete for good jobs in today’s global economy. Highly skilled workers in the U.S. are becoming harder to find, which opens the doors for foreign workers to fill those roles.

Business Week points out the fact that more Chinese students are earning their MBA’s and finding work in skilled positions like data scientists, engineers, software developers, and more.

To compete for these jobs, post-secondary education is as important as ever for American students. However, when faced with high costs, we encourage students to plan carefully and get through college with as little debt as possible, and we hope we’ve helped you find a few good ways to do that today.

Image credit: “Girl with Books” by CollegeDegrees360/CC BY 2.0)

Featured Image Credit – COD Newsroom / CC BY 2.0

Related Articles

Six Ways Online Schools Can Support Military Families

A Parent’s Guide to Switching Schools Midyear

How to Make Summer Reading Fun This Summer: 11 Ideas Kids Will Love

Top Four Reasons Families Are Choosing Online School in the Upcoming Year

AI in Education: Exploring the Benefits and Challenges

Get your plans organized with our new daily and monthly planners

Your Guide to Homeschool Success

Is your kid struggling in school? Practical steps to turn things around.

Prevent Learning Loss With Educational Summer Activities for Kids

4 Inspirational Stories of Women Who Changed the World

Food Trivia for Kids: Fun Facts to Share at the Dinner Table

Beat the Summer Slide: Tips for Keeping Young Minds Active

Flexibility in Online Schooling: A Smarter Way to Learn

How Tutoring for Math Can Turn Struggle Into Success

How Video Creation Helps Kids Find Their Voice

6 Reasons Southwest Families Are Choosing Online Education

Tips for Choosing the Right School for Your Child

Education Online? One Family’s Success Story

Must-Read Books for Your Home Library: The Best Books by Age Group

Lights, Camera, Creativity! How Kids Can Express Themselves Through Video

The Benefits of Online Learning for Early Reading Skills

Mastering Cooking Skills: How Kids Benefit in the Kitchen and the Classroom

How Am I Going to Pay for College?

National School Choice Week: What Parents Need to Know

A Parent’s Guide to Choosing a Great Tutor

Smart Goals for Students: Unlock Your Full Potential

3 Easy School Snack Recipes Every Parent Will Love

Writing Prompts for Kids to Spark Creativity: Fun and Engaging Ideas

Cooking Skills: Whisking Up Wisdom and Life Learning

5 Tips for Helping Your Kid Learn Cooking Skills (Without turning your kitchen into chaos!)

How to Write an Effective Outline for High School Essays

6 Ways to Help Your Child Combat Test Anxiety

5 Expert Tips to Manage Academic Stress

How Robotics Opens Doors to Promising Careers

5 Reasons Families Choose Online School for Special Education

From Bored to Engaged: 7 Ways Game-Based Learning Keeps Your Child Motivated

Should Parents Help with Homework?

Helping Your Military Kids Thrive: Navigating Their Unique Challenges

Study Smarter, Not Harder: 9 Ways to Make Studying More Fun

Helping Your Teen Craft Their First Resume: A Parent’s Guide

Six Ways Online Learning Transforms the Academic Journey

Encouraging Kids to Love Writing: Fun Activities to Spark Creativity

Turn Up the Music: The Benefits of Music in Classrooms

A Parent’s Guide to Managing and Reducing Student Stress

5 Factors That Affect Learning: Insights for Parents

Navigating the College Application Process: A Timeline for High School Students and Their Parents

Can Homeschooled Students Play School Sports?

Enhance Your Student-Athlete’s Competitive Edge with Online Schooling

Preparing for the First Day of Online School

Why Arts Education is Important in School

5 Ways to Start the School Year with Confidence

Tips for Scheduling Your Online School Day

The Ultimate Back-to-School List for Online and Traditional School

Best Children’s Audiobooks Free

Easy Science Experiments For Kids To Do At Home This Summer

5 Strategies for Keeping Students Engaged in Online Learning

How Parents Can Prevent Isolation and Loneliness During Summer Break

Gifts for Teachers

Countdown to Graduation: How to Prepare for the Big Day

5 Major Benefits of Summer School

Types of Poems

A Parent’s Guide to Tough Conversations

From Books to Tech: Why Libraries Are Still Important in the Digital Age

The Evolution of Learning: How Education is Transforming for Future Generations

The Ultimate Guide to Reading Month: 4 Top Reading Activities for Kids

30 Questions to Ask at Your Next Parent-Teacher Conference

Is Your Child Ready for Advanced Learning? Discover Your Options.

Your Ultimate Guide to Holiday Fun and Activities

Good Reasons to Switch Classes in Middle School

Building Strong Study Habits: Back-to-School Edition

Dual Enrollment: Getting a Jump on College

Early College Programs Give Students a Jumpstart